Open USD is a distribution play for the next dollar standard: against Circle’s float, bank-controlled rails, and the emerging market for machine payments.

On June 30, a consortium of more than 140 announced partners, including Visa, Mastercard, Stripe, BlackRock, Coinbase, Google, Standard Chartered, and a long roster of banks, fintechs, and crypto-native firms, unveiled Open USD (OUSD), a new stablecoin issued by an independent entity called Open Standard. Circle's stock fell 16% that day, and the coverage settled into a familiar frame: a new consortium challenging the 800-pound stablecoin gorilla.

That frame is incomplete. There is a distribution war here, fought on two fronts: one against incumbent stablecoin issuers for the float, and one against the banks for the rails. But there is also a third dimension: an option on machine payments, specifically the permissionless, machine-native settlement that the banks' account model cannot reach and USDC is not positioned to win. Together, they make OUSD far more than just another stablecoin.

The Design Is the Strategy

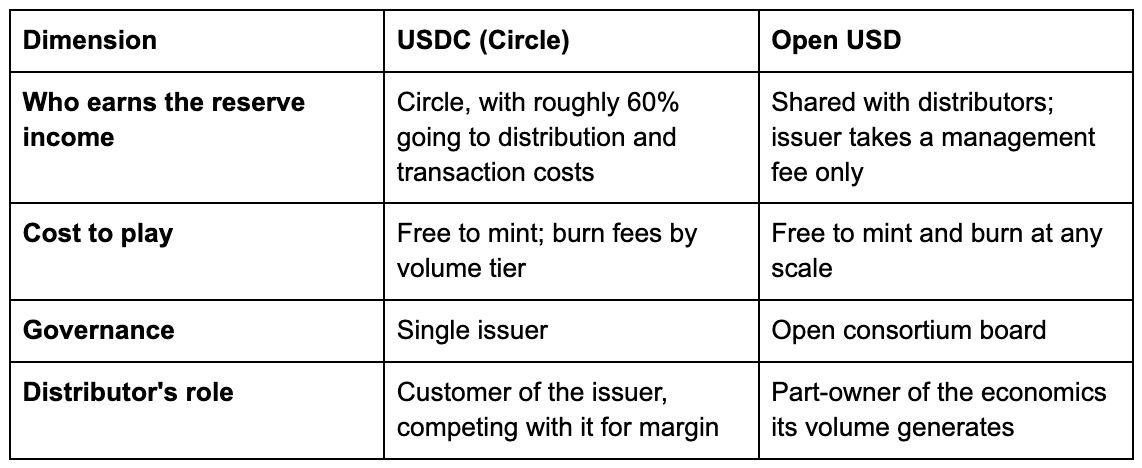

Start with the mechanics. OUSD charges nothing to mint or burn at any scale, and after a small management fee, nearly all reserve income flows to the partners who put the token into circulation. That is not a feature aimed at any single use case. It is a distribution-economics weapon, built to take float share from USDC and USDT.

The launch details point in the same direction. OUSD goes live first on Solana, Stellar, Base, and Polygon, with Stripe's Tempo to follow. The partner mix is a commerce and cross-border coalition: card networks, global banks, asset managers, marketplaces, fintechs, and crypto-native platforms.

The enabling mechanic is regulatory, but OUSD is not inventing it from scratch. Stablecoin issuers cannot pay yield directly to holders, but they can share economics with the platforms that distribute and support transactions in the token. Circle already does this through distribution and transaction costs, much of it tied to partners such as Coinbase. OUSD’s move is to make that bargain explicit: reserve income is not the issuer’s margin to defend, but the distributor’s incentive to adopt.

Front One: Taking the Float from Issuers

Circle's exposure is not USDC the product. It is issuance as a profit center. Every large distributor now negotiates with a credible alternative in hand, starting with Coinbase, whose revenue-sharing agreement with Circle comes up for renewal in August.

Circle CEO Jeremy Allaire's bear case deserves a hearing. Network effects favor the incumbent: USDC has seven years of integrations and deep liquidity. Free minting and burning could starve the infrastructure, because payment systems require ongoing investment that a thin management fee may not fund. Finally, stablecoin consortiums have a poor track record. USDC itself was born from Centre, a consortium with Coinbase that Circle later dissolved after shared governance proved ineffective. ARK's Lorenzo Valente notes that coordination among 140 rivals has no working precedent, while Paxos's Global Dollar ran a similar yield-sharing playbook in 2024 without denting the incumbents.

The rebuttal works on the same three terms.

First, network effects are shifting from issuers to distributors. USDC has deep integrations, but exchanges, wallets, fintechs, and venues increasingly decide which dollar sits closest to the user. Circle's May deal with Hyperliquid already showed distributors gaining bargaining power. OUSD formalizes that power and makes it portable.

Second, free minting and burning does not mean unfunded infrastructure. It means the operator monetizes the network layer rather than the entire float. Visa works in a similar way: issuers and acquirers earn much of the economics that drive distribution, while Visa charges assessment and processing fees for rules, compliance, brand, risk, and network operations. For OUSD, reserve yield is the interchange equivalent; the management fee is the assessment.

Third, a poor consortium history does not prove the model is wrong. It proves incentives must be explicit. OUSD's economic bargain is incentive alignment: partners are not joining to build a new issuer; they are joining to reclaim the reserve economics their own platforms create.

Front Two: Competing with Bank-Controlled Rails

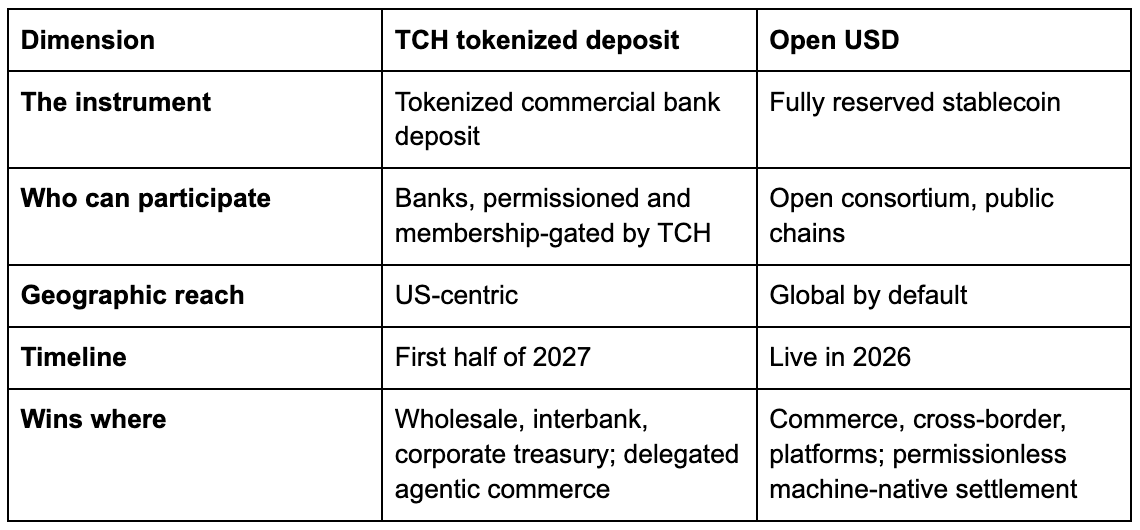

The big banks are building the opposite design: a shared tokenized deposit network operated by The Clearing House (TCH), led by JPMorgan, Citi, Bank of America, and Wells Fargo, and targeting the first half of 2027. Permissioned, US-centric, and settling claims on the issuing bank, it is the closed mirror image of a stablecoin like OUSD.

Line up the two rosters and it looks like a clean split. Of the seventeen TCH banks, only four also appear on the OUSD list, and the four ringleaders are absent entirely. The banks that did join OUSD are almost all foreign, including DBS, Standard Chartered, BBVA, OCBC, UOB, ANZ, Westpac, Mizuho, and Itaú. These are precisely the institutions a US-only network excludes by design.

But look at what the overlap banks are doing, not which side they are on. The tell is BNY, the world's largest custodian, which already holds USDC's reserves for Circle. It joined OUSD in the same role it plays everywhere: custody, not allegiance. The token layer is contested and geographic. The infrastructure layer beneath it is neutral, and gets paid whichever dollar wins.

Both camps are chasing agent payments, but not the same kind. The timeline is the pressure point: OUSD is live this year, while the banks' network is expected six to twelve months later. Standards races are won on integrations, not feature comparisons, and the open standard is spending its head start recruiting them.

Front Three: Becoming the Machine-Payments Dollar

The machine-payments stack around Stripe has three layers. Tempo is the rail: a blockchain built for fast, low-cost stablecoin settlement. MPP is the application layer: an HTTP 402-based protocol that lets agents discover prices, authorize payments, and pay for digital resources without requiring a traditional account, API key, or human approval for each transaction. OUSD is the settlement asset: the dollar instrument designed to move through that stack. Tempo moves value, MPP coordinates the transaction, and OUSD is the money.

The distinction that matters is between two kinds of agent payment. In delegated commerce, the agent spends its principal's money and rides an existing account. It is still tied to a customer, and banks can serve it natively. The second pool is permissionless and machine-native: an API charging a scraper a fraction of a cent, one model paying another per inference, across borders and around the clock. It is not a bank customer and cannot hold a banks-only, US-centric deposit token. It needs a bearer instrument on a public chain. That pool is what open stablecoins and MPP are built for.

Against USDC, the edge is narrower but still real. OUSD is aligned with Stripe’s machine-payments stack, and it gives platforms a direct economic reason to push volume through it. In markets where defaults are set by distribution, being early and sharing the economics with integrators is how a standard gets formed.

The Infrastructure Opportunity

Issuance is commoditizing, and value is migrating to the layers beneath it: liquidity across tokens and chains, on- and off-ramps in the corridors that matter, orchestration that selects the right instrument for each transaction, and the compliance machinery around all of it. A world with one more major stablecoin, a bank network arriving behind it, and a possible new class of machine-initiated volume is a world with more conversion, routing, and settlement complexity. That complexity is where the infrastructure layer earns its keep.

The deeper lesson from Stripe's strategy is about standards, not tokens. Its entire play, from HTTP 402 to an open consortium coin to public chains, is a bet that payments will be won on interoperability and developer adoption, not proprietary control. Historically, the rails that scaled, including TCP/IP, EMV, and ACH, won by being open enough for others to build on them. A provider whose payments stack is wired to a single issuer's token, one chain, or one company's reference implementation is rebuilding the gated design the market just voted against. Supporting open standards natively is no longer the enlightened option. It is table stakes for staying in the flow.

The right posture, then, is early, neutral integration: support OUSD alongside other stablecoins and deposit tokens, and treat the instrument and the rail beneath it as a per-transaction routing decision rather than an architectural commitment. Enterprises will want a counterweight to any single author's stack, however open its branding.

The question is not which dollar wins. It is who routes every dollar, across issuers, deposit tokens, public chains, and machines. That is where the next layer of payments power will sit.